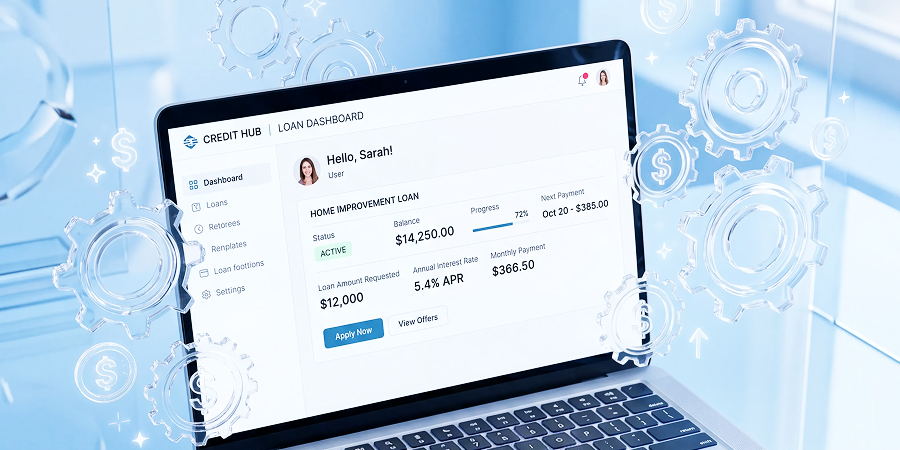

Custom finance software

Financial software development services covering the full BFSI stack — fintech, lending, payments, and RegTech.

Cross-industry engineering experience across regulated and high-growth sectors.

All Industries

“The global neobank market is projected to reach $2.05 trillion in transaction value by 2030.” — Statista

“Banking-as-a-Service revenue is projected to reach $38 billion globally by 2027 as neobanks and fintechs accelerate adoption of licensed banking infrastructure.” — BusinessWire

USA

USA PL

PL UA

UA MX

MX TR

TR

Neobank app development is the engineering of digital-only banking platforms delivering financial services exclusively through mobile apps and web — with no physical branches. It differs from traditional banking app development in architecture: neobanks use API-first microservices, BaaS providers for regulated banking infrastructure, and cloud-native stacks. Core neobank app features include digital KYC onboarding, real-time payments, virtual card issuance, open banking integration, and embedded finance products.

Neobank app development cost depends on launch model, feature scope, BaaS provider, and compliance requirements. A BaaS-accelerated neobank build using Mambu or Thought Machine Vault as the banking core typically costs less than a fully custom neobank from scratch. White label neobank app development is the lowest-cost path to market. Zoolatech provides a detailed scoping estimate after a discovery session mapping your product vision and regulatory position.

Not always. Most neobanks use a BaaS model — partnering with a licensed bank via Synapse, Solarisbank, or Railsbank — to access regulated banking infrastructure without holding a full banking license. This is the fastest and lowest-capital path to launch. Applying for a full banking charter is an option for larger neobank operations wanting full control over banking services and regulatory relationships.

Banking-as-a-Service is a model where a licensed bank provides banking infrastructure — accounts, cards, payment rails, and compliance — via API to neobanks and fintech companies. Instead of obtaining a banking license, a neobank integrates with a BaaS provider to deliver regulated banking services under the provider’s license. This reduces neobank app development time from years to months and eliminates the capital requirements of a banking charter application.

A BaaS-accelerated neobank with core features — KYC onboarding, accounts, transfers, and card management — typically takes 6 to 10 months from discovery to production launch. A fully custom neobank from scratch with proprietary banking infrastructure, multi-currency, BNPL, and AI features runs 12 to 18 months. White label neobank app development can reach MVP in 3 to 6 months. Timeline is heavily influenced by BaaS provider integration complexity and regulatory approval requirements.

Neobank app features Zoolatech builds include digital KYC and AML onboarding, real-time payment rail integration, virtual and physical card issuance, multi-currency account management, spending analytics, savings automation, BNPL integration, embedded insurance and investment products, open banking API connectivity, and AI-driven credit scoring. Feature scope is defined during the discovery phase based on target customer segment, launch model, and neobank app development cost parameters.

Yes. White label neobank app development covers pre-built neobank modules with custom branding, feature selection, and API-first customization — the fastest path to market for regional banks launching digital subsidiaries or fintech companies validating a neobank concept before committing to a full custom neobank build. Zoolatech delivers white label neobank solutions with the same compliance engineering standards applied to fully custom neobank development projects.

The primary differentiators are BaaS integration expertise across Mambu, Thought Machine Vault, Solarisbank, Synapse, and Railsbank — and compliance engineering that maps KYC, AML, PSD2, and GDPR requirements at the architecture stage rather than post-development. Combined with ISO 42001-governed AI features, 60% senior engineers, and a structured neobank app development process, Zoolatech operates as a long-term neobank development partner accountable for platform outcomes.