Custom finance software

Financial software development services covering the full BFSI stack — fintech, banking, payments, and RegTech.

Cross-industry engineering experience across regulated and high-growth sectors.

All Industries

“The global digital lending platform market is projected to reach $44.5 billion by 2030, growing at 27.7% CAGR.” — Grand View Research

Digital application intake, underwriting automation, and credit decisioning

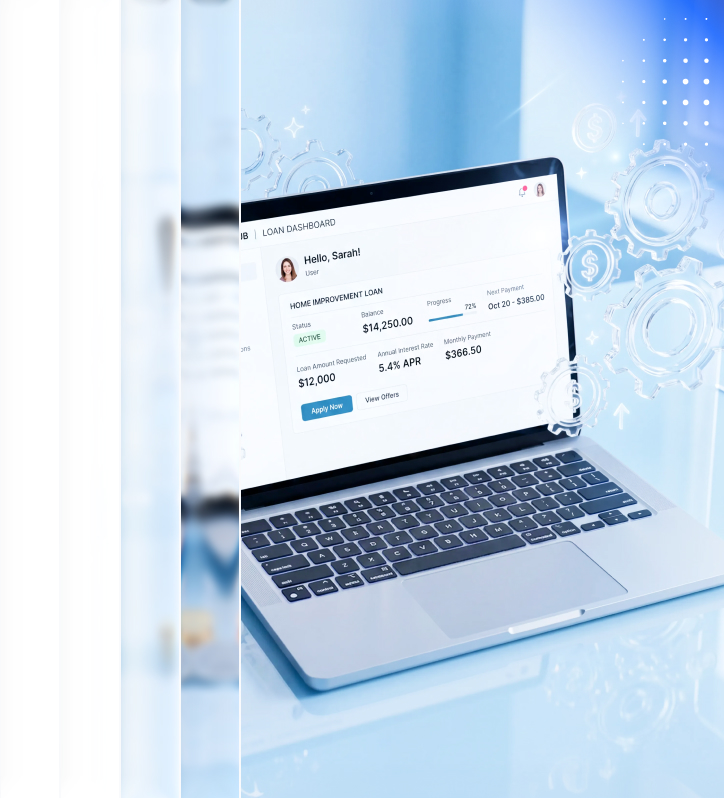

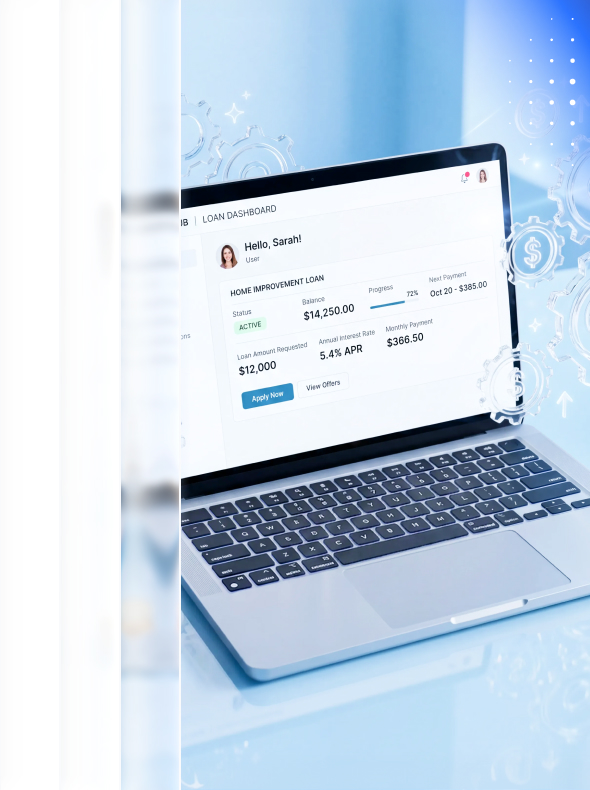

Loan servicing, payment processing, and portfolio management

Borrower and investor marketplace with automated loan servicing

Installment payment engines, lending management, and integration for digital lending software products

Loan origination, underwriting automation, and closing workflow

AI-powered credit scoring, explainable decisioning, and fraud detection

Auto loan origination, dealer integrations, and financing automation

“AI-powered credit decisioning reduces loan origination costs by up to 40% and improves credit risk assessment accuracy by 25% compared to traditional scoring models.” — McKinsey & Company

USA

USA PL

PL UA

UA MX

MX TR

TR

Lending software development is the engineering of digital systems that automate the full loan lifecycle — from borrower application and credit assessment to underwriting, loan servicing, payment collection, and compliance reporting. It covers loan origination systems, loan management software, P2P lending platforms, BNPL platforms, mortgage software, and credit decisioning engines. Lending software must comply with TILA, ECOA, RESPA, HMDA, and state-specific lending laws.

Custom lending software types include loan origination software for digital application intake and underwriting automation, loan management systems for servicing and payment collection, P2P lending platforms with borrower and investor marketplace functionality, BNPL installment payment engines, mortgage software covering URLA and HMDA compliance, credit decisioning engines with alternative data and explainable AI, and debt collection software meeting FDCPA requirements.

Lending software Zoolatech delivers is designed for TILA APR disclosure and Reg Z requirements, ECOA and Reg B fair lending with explainable AI for adverse action compliance, RESPA mortgage settlement disclosures, HMDA loan data reporting, FDCPA debt collection communication rules, Dodd-Frank qualified mortgage standards, and state-specific usury laws and licensing requirements across US jurisdictions. Compliance requirements are mapped at the architecture stage — not added post-development.

AI improves lending software in three areas: credit scoring using ML models with alternative data including cash flow analysis and open banking data for better risk prediction than FICO alone; document processing using LLM extraction from pay stubs, tax returns, and bank statements to reduce manual review; and fraud detection using synthetic identity scoring and application fraud models. All credit AI systems Zoolatech delivers operate under ISO 42001 governance with explainability for ECOA fair lending compliance.

A focused lending module — borrower portal, LOS integration, or credit bureau connectivity — typically takes 3 to 6 months. A full lending platform covering LOS, loan management systems, and credit decisioning engine runs 9 to 18 months. A P2P lending platform takes 12 to 18 months. Lending software development cost depends on solution type, compliance scope, integration complexity, and AI credit model requirements. Zoolatech provides a detailed estimate after a discovery phase mapping regulatory scope and the full integration map.

Yes. Zoolatech developed and optimized a scalable P2P lending marketplace for Credible — architecting the platform to handle high transaction volume with automated lender matching and loan processing automation. Zoolatech also built the Credible Lender Autopilot, which reduced loan processing from days to 1–2 minutes through automated lender integrations. Five published lending platform cases across consumer lending, P2P lending, digital lending, and AI-powered lending automation are available on the Zoolatech case study page.

The primary differentiators are 5 published lending platform cases with measurable outcomes, compliance-first engineering that maps TILA, ECOA, RESPA, and HMDA at the architecture stage, and ISO 42001-governed AI credit scoring that meets ECOA explainability requirements. Combined with 60% senior engineers and full-stack delivery covering LOS, loan management software, credit bureau integrations, and payment rails in a single lending app software development company engagement, Zoolatech operates as a long-term lending software development partner accountable for platform outcomes.

Yes. Legacy loan management system modernization at Zoolatech uses a phased migration approach — incrementally replacing legacy lending software components while keeping the existing system live during validation. This eliminates the risk of a single cutover that disrupts active lending operations. Modern lending software development for legacy replacement covers loan servicing software re-architecture, credit bureau integration updates, compliance framework alignment, and cloud-native infrastructure migration. Every lending app development project of this type is delivered under the same compliance-first engineering standards as new platform builds.